Fewer employers are offering workers supplemental health benefits for retirement; those that do increasingly push Medicare Advantage

Fewer employers are offering workers supplemental health benefits for retirement; those that do increasingly push Medicare Advantage

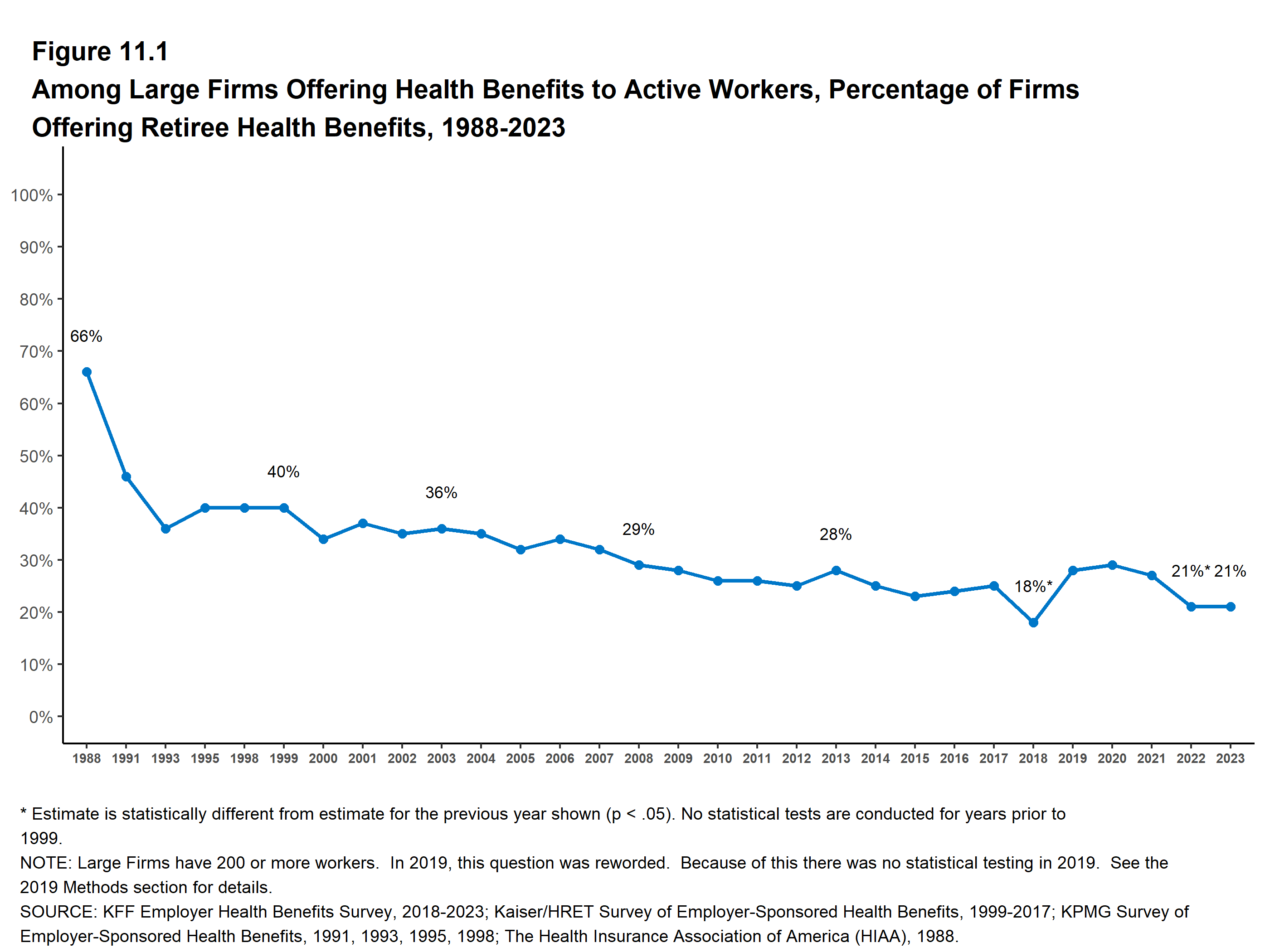

A new analysis from the Kaiser Family Foundation (“Retiree Health Benefits: Going, Going, Nearly Gone?”) reveals a marked decline in supplemental employer-provided retirement health benefits. Across 5 surveys, the share of Medicare-Age adults with supplemental retiree benefits has fallen dramatically over the past few decades. Today, only 12-21% of older adults have such benefits.

Source: KFF

Over a longer time course, the reduction is even more striking: in 1988, 66% of large employees offered workers retiree health benefits, which was down to 21% in 2023

Source: KFF

{kind=link}

Supplemental health benefits are valuable to seniors because, while retirees will generally be eligible for Medicare upon turning 65, that program has limits in the scope of coverage (e.g. little coverage for dental, eye care) and substantial cost-sharing. The KFF analysis notes several potential reasons for the decline in these benefits, such as declining union membership.

A parallel and equally notable development has been that, among employers who do continue to offer retiree health benefits, a rising share do so through Medicare Advantage group contracts, rather than (for instance) by providing supplemental “Medigap” plans that fill the gaps in traditional Medicare:

Source: KFF

A prominent recent example of an attempt by an employer to swap out supplemental benefits in favor of Medicare Advantage for retirees took place last year in New York City; the shift would have affected some 250,000 retired workers. Retirees would have lost their traditional Medigap benefits, which cover gaps in coverage in traditional Medicare, and instead be enrolled in a privatized Medicare Advantage plan run by Aetna. New York City municipal workers fought the change, which would have limited their access to providers because, unlike traditional Medicare which is accepted by basically all major hospitals, Medicare Advantage plans use provider networks that exclude major institutions, and have other barriers to care e.g. greater use of prior authorization. However, the Manhattan Supreme Court ultimately stopped the city’s plan.

There are several takeaways here. First, the shift among employers to offer retirement health benefits only in the form of Medicare Advantage plans is likely contributing to the broader Medicare Advantage takeover (In 2023, for the first time, Medicare Advantage enrollment overtook that of traditional Medicare). Given that taxpayers significantly overpay insurers for their Medicare Advantage offerings relative to what they would pay for traditional Medicare benefits, this shift will weaken the financial foundation of the program. Second, the decline in retiree health benefit offerings by employers could drive increased household financial precarity for some Medicare participants; this, in turn, may further drive Medicare Advantage enrollment as retirees may be drawn to its lower out-of-pocket costs — at the cost of inferior access to care and providers which becomes most evident when we get sick.

There is an obvious alternative to this accelerating corporatization: eliminate Medicare Advantage, and use the savings (from reduced overpayments to insurers) to expand traditional Medicare in order to fully cover seniors’ health needs.